Gifts from Estate Plans

The most practical way to make significant gifts may be through your estate plan, by means of a will, living trust or beneficiary designation on a life insurance policy or retirement account. Such gifts are wholly revocable while you are alive and may save significant taxes for your estate.

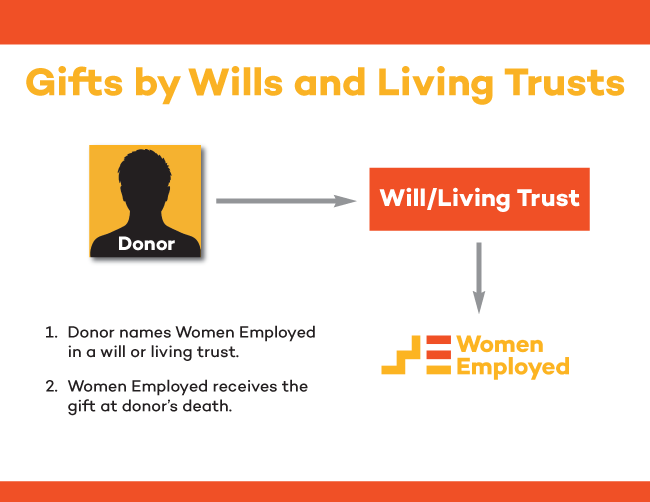

Wills and Living Trusts

A bequest is the most traditional way to provide significant help for worthwhile causes. With a gift through your will or living trust, you keep full use of your gift assets during your life. Some bequest language you can share with your adviser is located in Facts for Advisers.

You can structure a bequest in ways that will be both personally satisfying and tax advantageous. Charitable bequests take many forms:

Outright (specific) bequest.

This is a gift of a particular amount of money (for example: "I bequeath $25,000.").

Residuary bequest.

The residue of an estate is the amount

remaining after all specific bequests have been distributed; the

exact amount will not be known until the final accounting is completed.

The residue may pass as a percentage bequest (e.g., "I give one-third

of the residue of my estate.").

Contingent bequests.

You can name a secondary beneficiary

to receive property in the event the primary beneficiary is not

alive (for example: "I bequeath $10,000 to my father, but if he

has predeceased me, I direct the $10,000 be paid to . . . ").

Financial Accounts

Most accounts at financial institutions can be made payable on death

to a person or a charitable organization. Ask the manager of the

institution how you can arrange to designate a death beneficiary

for your CD, savings account, share accounts, etc. In some areas,

this is accomplished through a "P.O.D." (payable on death) designation.

Securities in a brokerage account can be left through a "T.O.D."

(transfer on death) designation.

Retirement Accounts

Your estate can save both income taxes and estate taxes if you make

a charitable organization beneficiary of part or all of your IRA

or other retirement account. Family members might keep only 30 cents

on the dollar, after taxes, from these assets. Changes in

IRS regulations have made it simpler and more favorable to name

worthwhile causes as beneficiaries of IRAs and other retirement accounts.

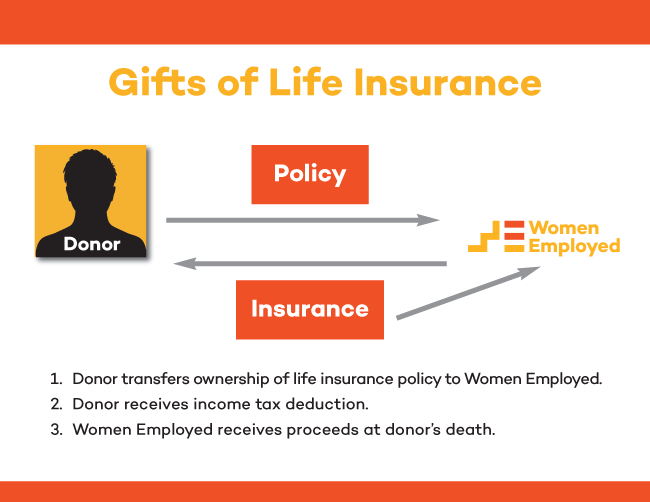

Life Insurance

You can name our organization as the beneficiary of a life insurance

policy (or a percentage of the proceeds) – just contact the company

for appropriate forms. A better idea may be to transfer actual ownership

of the policy to us (assuming it is a "surplus" policy that is no

longer needed for family security). Your gift will entitle you to

an income tax deduction, and any future premium payments will be

tax deductible.

Call us before . . . you make or amend your will, establish a living trust or name beneficiaries for pension plans and life insurance.