Donors wishing to retain payments for life from their IRA gifts can choose to fund a charitable remainder trust or charitable gift annuity with up to $50,000. This one-time option can be payable only to the donor and/or spouse. No other funds can be added to the remainder trust or gift annuity. All payments received will be taxed as ordinary income.

How Does the Law Let Me Increase My Gifts at No Cost?

IRA funds are heavily taxed whenever you draw them out, at rates as high as 39.6%. What’s more, the tax burden never goes away – even your heirs will pay income tax on IRA funds they receive from your estate, and federal estate taxes may apply, as well.

There is a satisfying alternative: Instead of sending so much tax off to Washington, DC, you can divert the tax collector’s “take” from your IRA to us.

Suppose you ordinarily send us a check for $1,000 every year. The table below shows that, instead of writing a check, you could instruct your IRA trustee to send us $1,333 (assuming you are in a 25% bracket). That $333 now can be used to advance our programs – and you will have increased your support by one-third, all paid for by the IRS.

Supercharge Your Support by Giving through Your IRA

If Your Anticipated Gift by Check Would Have Been:

|

$100 |

$500 |

$1,000 |

$5,000 |

$10,000 |

Your Highest

Tax Bracket |

You Can Increase to This Amount for Free by Giving through Your IRA* |

15% |

$117 |

$588 |

$1,176 |

$5,882 |

$11,764 |

25 |

133 |

666 |

1,333 |

6,666 |

13,333 |

28 |

139 |

694 |

1,390 |

6,944 |

13,888 |

33 |

149 |

746 |

1,490 |

7,462 |

14,925 |

35 |

153 |

769 |

1,538 |

7,692 |

15,384 |

39.6 |

166 |

828 |

1,656 |

8,278 |

16,556 |

*To calculate different IRA gift amounts than those shown, simply divide your normal gift amount by 1.0 minus your tax bracket. For example a person in the 28% bracket who usually gives $1,200 could give $1,200 ÷ .72, or $1,667, through an IRA at no additional cost. Donors who can “itemize” deductions for their gifts will have somewhat different tax results from those shown in the table, but may also reduce various penalties linked to a taxpayer’s adjusted gross income by substituting IRA gifts for cash contributions. |

|

Gift Ideas with Your IRA

-

Significant Gifts. Phyllis has planned to leave us most of her IRA at her death, but wishes she could see her gift at work now, during her lifetime. Phyllis plans to direct a $100,000 gift from her IRA and avoid both income taxes and estate taxes.

-

Annual Distribution Gifts. Roberta, for example, must withdraw $20,000 from her IRA, even though she doesn’t need the money for living expenses. If Roberta wishes, she can direct a $20,000 transfer to us prior to taking any distribution and reduce her federal taxes by $5,600 in her 28% tax bracket.

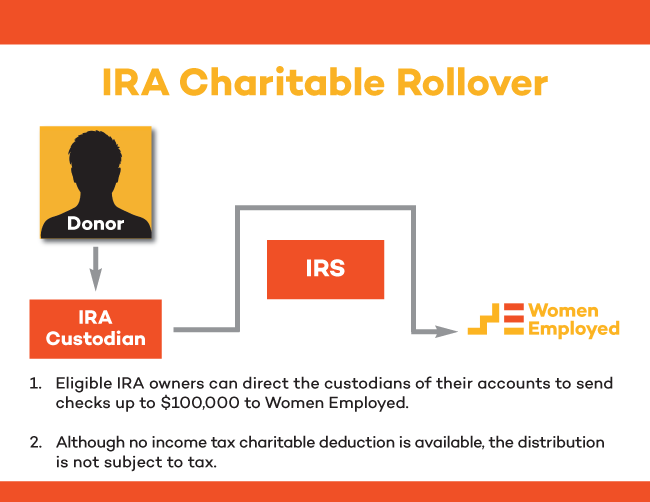

IRA Gift Rules

-

Donors must be past the age of 70½ and own a traditional or Roth IRA – other retirement plans such as pensions, 401(k) plans and others are not eligible.

-

Only the IRA trustee can transfer gift amounts to a qualified organization. If IRA owners withdraw funds and then contribute them to charity separately, amounts withdrawn will be included in the donor’s gross income.

-

No charitable deductions are allowed, but gift amounts will not be included in donors’ incomes.

-

IRA gifts may not exceed $100,000. The “ceilings” on contribution deductions (50% of adjusted gross income for cash, 30% of AGI for long-term capital gain property) do not apply to IRA gifts.

-

Transfers are not permitted to donor advised funds, private foundations or supporting organizations.

-

IRA gifts cannot be made to charitable remainder trusts or other “life income gift” arrangements.

To make an IRA gift, just contact the trustee of your account. Please call our office if you plan to make a gift from your IRA so we can ensure proper transfer of your gift and provide the substantiation you’ll need.

IRA Gifts Have Special Appeal for:

-

Donors who have an IRA and are over the age of 70½. Even those who don't need to take required minimum distributions until age 73 (IRA owners turning 72½ in 2020 or later), may make qualified charitable distributions from IRAs. Other retirement accounts, such as 401(k) plans, are not eligible, although it may be possible to roll over these plans into IRAs and then make qualified IRA gifts.

-

Donors who use the standard deduction. Income tax deductions are not available for IRA contributions, but gifts are exempt from all federal taxes, which may be important to donors who do not itemize their deductions. IRA gifts make a detour around the tax collector, so donors who don’t itemize won’t need a charitable deduction to offset taxes.

-

Friends who wish to avoid tax on required minimum distributions. IRA gifts will count toward the minimum distributions required of individuals over age 70½ and reduce their taxes. Important: this tax break generally won’t be available if you have already received your minimum distribution for the year. Be sure to make your IRA gift before taking a required distribution.

-

People who want to reduce taxes on their estates. IRAs are subject to both income taxes and estate taxes after the owner dies, resulting in overall taxes of 60% or more. Making qualified IRA gifts avoids these taxes.

-

Donors who can’t deduct all their contributions. The most a person can deduct for charitable gifts in any year is 50% of AGI (excess deductions can be carried over for up to five years). But gifts made directly from IRAs aren’t considered under this 50% limitation, which allows extra tax benefits for friends who wish to make large gifts this year.

Are You Too Young for IRA Giving?

For many years, advisers have been telling people that retirement accounts are the very best thing to leave to worthwhile organizations in their estate plans. A combination of death taxes and state and federal income taxes can take 60% or more of the retirement accounts of many people at death, leaving little remaining for heirs.

People of any age can name us as partial or 100% death beneficiary of an IRA, 401(k) or 403(b) plan or other retirement account and avoid taxes. You also can leave your retirement account to a trust that will pay income for life to a spouse or family member, with later benefit for our programs. Contact us for full details.